This news article is more than 12 months old and some of the information may be out of date - please see our latest news articles here.

How to reduce the supply of rented homes: introduce Rent Controls!

Introduction

The issue of rent controls in the Private Rented Sector (PRS) has considerable policy interest. Ongoing concerns about affordability in housing have been compounded by rising inflation and a wider cost-of-living crisis. Among politicians, rent controls appear to be a panacea:

- In 2022, the Scottish Government introduced legislation to freeze rents for private and social tenants, later amending this to cap increases during tenancies to 3%.

- The Welsh Government has recently published a Green Paper Consultation exploring fair rents.

- In England, several mayors, most notably the Mayor of London, have proposed rent controls as a solution to address housing affordability challenges.

Although rent control policies aim to provide stability and affordability for tenants, analysis suggests that rent controls are a poor instrument to achieve these goals and often result in unintended consequences. This blog post focuses on the views of landlords towards rent controls and what the impact of such controls would likely be.

Different types of rent controls

Rent control policies have evolved over time and can be split into three broad categories:

i) First generation rent controls – This entails a form of 'hard' control in which rents are fixed and remain frozen. Put simply this means rents have a maximum price ceiling.

ii) Second generation rent controls – rent increases are limited to a set percentage or pegged to inflation.

iii) Third generation rent controls – these allow initial rents (i.e., new tenancies) to be freely set by landlords or with a very light restriction but limit rent increases within tenancies.

Unintended consequences

Compelling evidence demonstrates that where rent controls policies have been enacted in regions around the world, they have failed to offer an effective solution to address housing affordability challenges.

Instead of tempering rising rents, research has shown they fail to address the underlying issues of affordability. Unintended consequences include:

- Reduction in market supply due to landlords selling properties and exiting the market.

- Reduced incentives for landlords to invest in property upgrades and maintenance.

- Regulatory failings around capacity to enforce rent controls and a lack of consistency in enforcement.

- The emergence of labour market rigidities: Tenants in properties under rent controls remain in those properties for longer periods. This has a detrimental effect on newer entrants to the market. Potential newer entrants - often younger renters - find themselves 'locked out' of rent controlled areas.

Landlord views on rent controls

This blog post draws on findings from a YouGov landlord poll of over 1,000 landlords across England & Wales. The survey was commissioned by the NRLA in Winter 2022 across England & Wales. Around 10% (9.6%) of these landlords were members of the NRLA.

Among the topics discussed in the survey was landlord sentiment towards second and third generation rent control. Landlords were asked to comment on the following three scenarios:

Scenario 1 - Rents are fixed by an external authority both during and between tenancies (second generation)

Scenario 2 – Rent increases are pegged to inflation both between and during tenancies (second generation)

Scenario 3 – Rents for new tenancies are set by landlords but subsequent increases are limited to inflation or set by an agency (third generation)

Landlords were asked how they would respond to each rent control scenario. For each scenario, the largest grouping of landlords stated the rent control measure would not make any difference. These landlords will continue to let property as before under these rules. There are however some differences in the sizes of this group in the respective scenarios - see Figure 1 below:

The above results show that Scenario 1 received the most pushback from respondents.

Scenario 1 and Scenario 2 are similar in that they restrict landlords from setting the rent at any point. The key difference is that landlords are even less receptive to the idea of rents being set by an external authority compared to a simple inflation-based rent peg.

- Figure 1 reveals landlords were much less likely to carry on letting as previously in Scenario 1 (39% stating there would be no difference) than in Scenario 2 (61% stating there would be no difference).

- The reluctance to have an external authority setting rents is confirmed in the third-generation Scenario 3.

- In this case, even though landlords set initial rent, the prospect (even on the either-or basis outlined) of an external body setting rents during a tenancy seems enough to repel landlords.

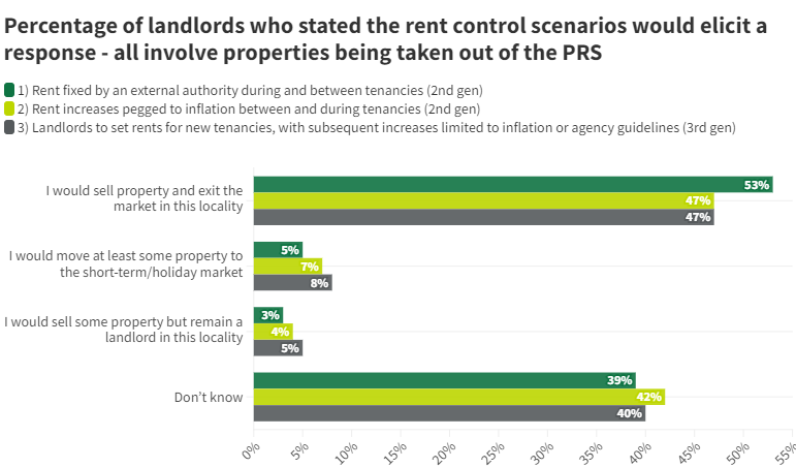

How landlords would respond to rent controls

Those landlords who WOULD make a change were asked what changes they would implement. This means that the percentages below reflect a larger number, as well as a larger proportion of landlords for Scenario 1 (where Figure 1 shows a far smaller proportion of landlords "carrying on" under the proposed regime).

Chart 1: The changes landlords would instigate

Chart 1 shows how those landlords who would change behaviour could react to the scenarios posed above. It is Scenario 1 in which one would anticipate the highest proportion of landlords selling all their properties in that locality and exiting the market.

- Over half (53%) of the landlords who would act in response to rent controls indicated that they would sell their properties in the affected area and exit the market in that locality.

- For Scenarios 2 and 3, this figure was slightly lower at 47%.

If those responding "carry on as before" are re-included, the results still indicate a significant impact on the PRS:

- In Scenario 1, 37% of all landlords would seek to reduce the number of properties available to let in the PRS.

- In Scenarios 2 and 3, this proportion falls: however, it remains the case that more than one-landlord-in-five stated they will be reducing housing supply in the rent control area.

Furthermore, as Chart 1 above shows, a large proportion of landlords remain "Undecided". If even a few of this undecided group act to reduce their portfolios in the rent control area, the problem of supply is exacerbated.

A lesson from Scotland

As a response to affordability challenges posed by the impact of Covid-19 and the wider cost-of-living crisis, Scotland introduced temporary rent controls.

- The Cost of Living (Tenant Protection) Scotland Bill (2022) capped mid-tenancy rent increases to 0% until 31 March 2023.

- On 1 April 2023, the rent price increase cap was increased to 3% (and up to 6% in certain circumstances).

- This third generation-model rent control only applies to in-tenancy rent increases. There is no restriction on rent increases for new lets.

Chart 2 below shows that rent increases in Scotland have followed the same trend as England – even though there are no rent controls in England. Note that the recorded rise in Scotland’s rents in this chart pre-date the April 2023 mandated increase.

Chart 2: Rent rises in England & Scotland

Conclusion

While rent controls appear to many as a simple solution to housing affordability challenges, they come with uninteneded consequences. Economists have presented detailed evidence to show rent control policies could lead to reduced market supply – as well as a range of other housing and labour market problems.

This YouGov market research underlines these supply-constraint concerns: if landlords are unable to meet rising costs, many will reduce their portfolios, exacerbating current PRS-supply difficulties. The result of rent controls will have significant consequences for the balance between supply and demand: irrespective of the chosen rent control model.