This news article is more than 12 months old and some of the information may be out of date - please see our latest news articles here.

Are rent arrear issues increasing for UK landlords?

As the UK continues to face a cost of living crisis, people across the country are likely to be cutting back on luxuries and other non-essential expenditures. Despite this, between rising energy prices and record-high inflation rates, some people may still be struggling to make ends meet.

As a result, there could be an increased risk of tenants being unable to make rent payments, leaving landlords with a loss of income.

How has the cost of living crisis affected rent prices?

As prices rise for a wide variety of products and services, the cost of rent has been no different. With interest rates rising sharply in 2022 and the first half of 2023, many homeowners were facing increased repayment costs when renewing their fixed-rate mortgages in 2023. The Bank of England stated that, from a survey carried out between 30th August and 19th September 2023, almost 40% of homeowners reported an increase in their mortgage rates in the previous year.

For private landlords, particularly those with interest-only mortgages, this may mean they have to increase the amount of rent they charge tenants to cover the cost of owning and running a rental property.

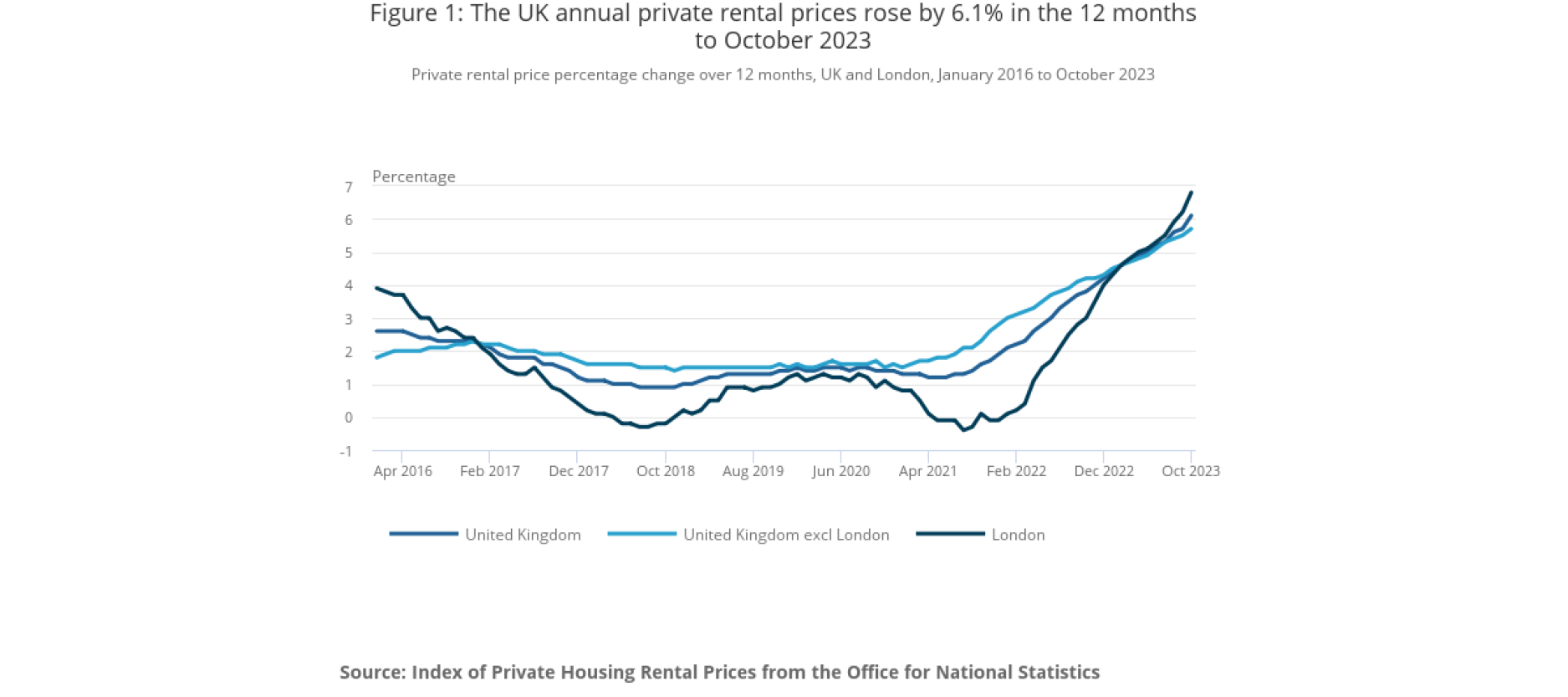

According to the Office for National Statistics (ONS), private rental prices in the UK rose by 6.1% in the 12 months to October 2023, which was up from 5.7% in the 12 months to September 2023. This figure was even higher in London with an annual increase of 6.8%.

During this period between October 2022 and September 2023, the ONS recorded the highest-ever median monthly rent in England at £850 per month.

Are household incomes failing to keep up with the cost of living?

Typically, wages or salaries are expected to increase regularly in line with inflation, since inflation leads to people needing more money to buy the same amount of goods compared to the previous year. However, as inflation rose steeply in recent years, wages in many sectors struggled to keep up.

According to ONS, as a result of the rising inflation rates in 2022: “regular wage growth fell behind inflation in all industries except professional and scientific (which includes businesses covering areas such as legal services, management, engineering and scientific research). In other industries, such as public administration and education, pay growth has been below inflation since the second half of 2021.”

It can be this disproportion that leads to people struggling to keep up with the cost of living, since their salary or wages do not go as far as they used to. Reports show that rising costs have put a strain on household incomes.

According to the JRF report A Minimum Income Standard for the United Kingdom in 2023: “A single person needs to earn £29,500 a year to reach a minimum acceptable standard of living in 2023. A couple with two children need to earn £50,000 between them.” Therefore, households falling short of these standards may be struggling to make ends meet. However anyone over the age of 22 who works 35 hours per week at minimum wage would only be receiving £18,964 (until the expected minimum wage increase in April 2024) more than £10, 000 below the £29,500 threshold.

The JRF outlines the struggles specifically faced by low-income households, stating: “In May 2023 we found that 7.3 million low-income households went without essentials in the first half of 2023, and 4.5 million were in arrears.”

This shows that many families and households aren’t just having to cut back on nice-to-haves like meals out or their Netflix subscription, but are also having to cut back on essentials in order to pay their bills or rent, and even then some are unable to do so.

How common are rent arrears in the UK?

The previous statistic suggests how common arrears may be among low-income households, which could include arrears relating to rent, mortgages or other loans. Similarly, a Guardian article from May 2023 states that around 700,000 households missed or defaulted on a rent or mortgage payment in the month prior. Another statistic claims that 36% of UK landlords faced rent arrears over a 12-month period.

These financial difficulties can then put renters at risk of eviction, as landlords can serve a Section 8 eviction notice to tenants with a minimum of two months of rent arrears. This may then leave tenants with the challenge of finding alterative accommodation, be that more affordable housing or staying with friends or family.

What help is available for tenants?

If your tenants are struggling to make their rent payments each month, there could be some support available to help them with the cost of living. Even if your tenants are employed, there may be some benefits that they are entitled to. For example, Universal Credit may be available for those on a low income who are struggling to pay the bills, as well as for parents or carers, among other circumstances. Your tenants can check if they are eligible and apply for Universal Credit here.

They could also use the entitled to benefits calculator or the Turn2us benefits calculator to help find out if they are eligible for any other kinds of benefits, or they can talk to a Citizens Advice advisor to help them learn more about the types of benefits available.

If your tenants are struggling with their bills, they could check if they are eligible for any council tax reductions. For example, if you rent to any single tenants, they may be able to get a 25% reduction on their council tax bill for living alone. Other factors that may make tenants eligible for a reduction include if they or someone they live with has a disability, or if they are on a low income or benefits.

Another option for tenants is a debt respite scheme called Breathing Space, which prevents landlords from taking enforcement action such as eviction for 60 days. During this time, the tenant should still make rent payments wherever possible, and they must seek debt advice in order to apply for Breathing Space.

Help protect your income with Rent Guarantee Insurance

Rent Guarantee Insurance can provide cover designed to help protect landlords from the financial losses that can occur as a result of tenants failing to pay their rent. This insurance can typically cover rent arrears and legal costs associated with the eviction of a tenant who has not paid their rent.

Rent Guarantee Insurance can help landlords in a few ways:

- By providing financial protection against unpaid rent, it can help to provide landlords with a financial backup if a tenant is unable to pay their rent.

- By covering the cost of eviction proceedings, it can help landlords through the process of evicting a tenant.

- By covering the cost of legal advice and representation, it can help landlords follow the correct procedures when evicting a tenant.

- As can be the case with any insurance policy, landlords should carefully review the terms and conditions to ensure the cover is suitable for their needs.

Rent Guarantee Insurance from Rentguard

With vast experience handling insurance policies for a wide range of landlords, and with relationships with a number of leading insurers, Rentguard Insurance aims to simplify your insurance arrangements and help to protect your property, its contents, and your liabilities.

Or speak to our specialist team on 0333 000 0169.

The sole purpose of this article is to provide information on the issues covered. This article is not intended to give legal advice, and, accordingly, it should not be relied upon. It should not be regarded as a comprehensive statement of the law and/or market practice in this area. We make no claims as to the completeness or accuracy of the information contained herein or in the links which were live at the date of publication. You should not act upon (or should refrain from acting upon) information in this publication without first seeking specific legal and/or specialist advice. Arthur J. Gallagher Insurance Brokers Limited trading as Rentguard and National Residential Landlords Association, an Introducer Appointed Representative of Arthur J. Gallagher Insurance Brokers Limited, accepts no liability for any inaccuracy, omission or mistake in this publication, nor will we be responsible for any loss which may be suffered as a result of any person relying on the information contained herein.

National Residential Landlords Association is an Introducer Appointed Representative of Arthur J. Gallagher Insurance Brokers Limited, which is authorised and regulated by the Financial Conduct Authority. Registered Office: Spectrum Building, 55 Blythswood Street, Glasgow, G2 7AT. Registered in Scotland. Company Number: SC108909. Rentguard is a trading name of Arthur J. Gallagher Insurance Brokers Limited.