What types of property damage can cost landlords the most to fix?

There are a range of costs to consider when managing a rental property, including those associated with maintaining the property. An unexpected accident, emergency or natural disaster can leave you in a tough spot. That’s why having suitable landlord insurance can help keep you covered and offers you a financial safety net.

One coverholder within Arthur J. Gallagher Insurance Brokers Limited* has shared the types of damage that can be most costly for landlords. This is according to claims data for tenanted property insurance policies taken out by 20,842 policyholders in 2023.

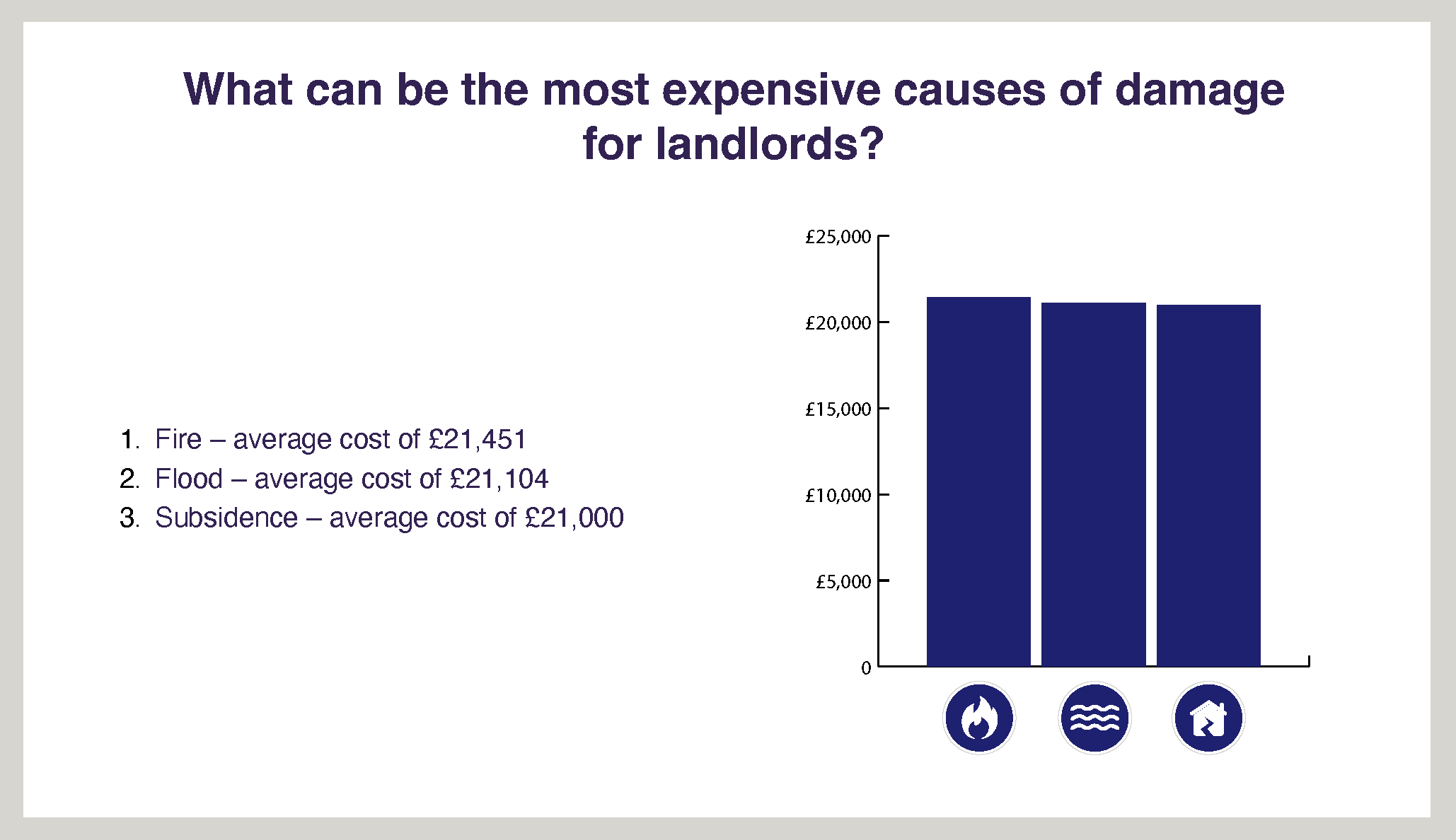

What can be the most expensive causes of damage for landlords?

According to the claims data, some of the most expensive insured causes of damage for tenanted properties in 2023 were*:

- Fire – average cost of £21,451

- Flood – average cost of £21,104

- Subsidence – average cost of £21,000

1. Fire damage

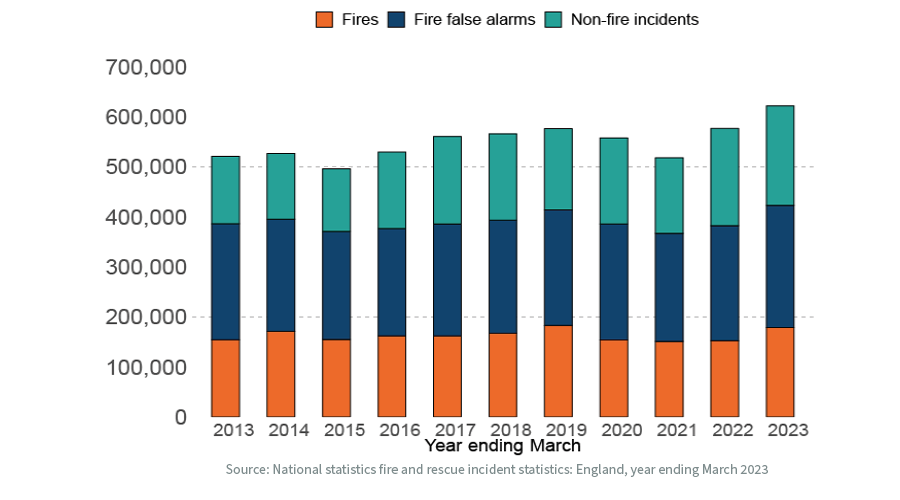

In the year ending March 2023, fire and rescue services in England attended 178,737 fires, which reflected a 17% increase compared to the previous year (152,639). Of these, 26,822 were primary dwelling fires, which refers to potentially more serious fires (as opposed to secondary fires) that occurred in residential properties.

As a landlord, it can be important to consider protecting both your property and your tenants from the risk of fire, as the year ending March 2023 saw 4,522 injuries and 203 fatalities caused by dwelling fires.

Landlords must follow fire safety regulations, including providing fire safe furnishings, access to escape routes, and a smoke alarm on each storey of the property. You may want to explain to your tenants the importance of regularly testing smoke alarms and detectors and replacing batteries when needed. This is also something you can check yourself during periodic landlord inspections.

Fire can cause devastating damage to both the building and its contents, and can leave your tenants without a habitable home. You may want to check your landlord insurance policy to check that you are covered against fire damage, and what that cover entails.

2. Flood damage

British weather can be unpredictable at best. And with the effects of climate change, extreme weather conditions such as floods and droughts are becoming even more common across the world. According to the Met Office, six of the UK’s ten wettest years on record have occurred since 1998. It also expects winters in the UK to become 30% wetter by the year 2070.

In October 2023, Storm Babet saw around 2,100 properties flooded across England and Wales, and Gov.uk claims that approximately 5.5 million homes and businesses in England are at risk of flooding.

Water damage to floors and walls can cause structural damage, while furniture, fixtures and fittings are also at risk. It can be important to understand your risk of flooding, as some areas and properties are more susceptible than others.

Gov.uk offers a free service that helps assess an area’s risk of flooding and provides advice on how to manage flood risk. Taking any necessary precautions and finding suitable landlord insurance could be important for your rental property.

3. Subsidence damage

When it comes to property insurance, subsidence refers to the downward movement or sinking of a building's foundation, causing it to settle unevenly. It occurs when the ground beneath a house loses stability or support, leading to structural damage.

House subsidence can be caused by various factors, including changes in soil moisture content, poor soil quality, tree root growth, or nearby excavation works. Signs of house subsidence may include cracks in walls, floors, or ceilings, sticking doors or windows, and uneven or sloping floors.

It is crucial to address house subsidence promptly to prevent further damage and ensure the safety and stability of the building.

House subsidence is a relatively common issue in the UK, particularly in areas with certain soil types or geological conditions. However, the frequency of house subsidence can vary depending on factors such as location, climate, and local geology. Some regions, such as parts of London and the southeast, are more prone to subsidence due to the presence of clay soils that shrink and swell with changes in moisture levels.

Homeowners should be aware of the potential risks and take necessary precautions to mitigate subsidence. Having suitable insurance in place can help to provide peace of mind that a financial safety net is in place.

Landlord insurance can help to cover a range of risks, including these potentially costly causes of damage. Landlords should always check their policy documents to be sure of the cover their insurance provides, as well as any conditions and exclusions.

Landlord Insurance from Rentguard

With vast experience handling insurance policies for a wide range of landlords, and with relationships with some of the leading insurers, Rentguard Insurance aims to simplify your insurance arrangements and help to protect your property, its contents, and your liabilities.

Or speak to our specialist team on 0333 000 0169.

*Claims data for the period 01/01/2023 - 31/12/2023 from Vasek Insurance’s Property Owners cover for tenanted properties, underwritten by Tokio Marine HCC. Vasek Insurance is a trading name of Arthur J. Gallagher Insurance Brokers Limited.

These risks are covered by Vasek Insurance’s Landlord Insurance product. Please refer to your own insurer’s policy wording for a list of covers and exclusions.

The sole purpose of this article is to provide information on the issues covered. This article is not intended to give legal advice, and, accordingly, it should not be relied upon. It should not be regarded as a comprehensive statement of the law and/or market practice in this area. We make no claims as to the completeness or accuracy of the information contained herein or in the links which were live at the date of publication. You should not act upon (or should refrain from acting upon) information in this publication without first seeking specific legal and/or specialist advice. Arthur J. Gallagher Insurance Brokers Limited trading as Rentguard and National Residential Landlords Association, an Introducer Appointed Representative of Arthur J. Gallagher Insurance Brokers Limited, accepts no liability for any inaccuracy, omission or mistake in this publication, nor will we be responsible for any loss which may be suffered as a result of any person relying on the information contained herein.

National Residential Landlords Association is an Introducer Appointed Representative of Arthur J. Gallagher Insurance Brokers Limited, which is authorised and regulated by the Financial Conduct Authority. Registered Office: Spectrum Building, 55 Blythswood Street, Glasgow, G2 7AT. Registered in Scotland. Company Number: SC108909. Rentguard is a trading name of Arthur J. Gallagher Insurance Brokers Limited.